To find out if someone has life insurance in the UK, start with three places: their paper documents and email inbox, their employer (for death-in-service benefit), and the Association of British Insurers' free tracing service at abi.org.uk. The ABI estimates more than £2 billion in unclaimed financial assets exist in the UK, much of it life insurance. Policies go unclaimed not because insurers keep the money, but because no one knew the policy existed. Roost's vault is built specifically for storing these details somewhere findable.

Why so much life insurance goes unclaimed in the UK

The most common reason life insurance is never claimed is simple: the beneficiary did not know the policy existed. Someone takes out a policy, mentions it once over dinner, and nobody records it. The insurer has no obligation to pay out unless a claim is made. The policy quietly lapses into the unclaimed assets pool.

A 2022 report from the Unclaimed Assets Taskforce, set up by the Association of British Insurers, estimated that more than £2 billion in insurance and investment products sits unclaimed in the UK. Much of this is life insurance taken out decades ago, often without a named beneficiary or with a beneficiary whose contact details have long since changed.

The second most common reason is outdated beneficiary details. Someone marries, divorces, or changes circumstances after taking out the policy and never updates the nomination. The insurer contacts the original named beneficiary, who may have died, moved away, or no longer have a connection to the policyholder's family.

Workplace death-in-service benefit is particularly commonly missed. This is not a separate policy the employee pays for — it is part of their employment contract, often worth three to four times their annual salary. Families who do not know it exists never think to claim it.

How to find out if someone has life insurance UK: 5 methods

These five methods cover the range of policies a person might have held. Work through them in order — the first two take an afternoon and cover most cases. The formal tracing services are for cases where paperwork and bank statements turn up nothing.

Method 1: Search their paperwork, email, and documents

Go through the deceased person's physical files and email inbox. Search for: life insurance, life assurance, term policy, whole of life, death benefit, critical illness cover, income protection. Most insurers issue annual statements and renewal reminders — even one of these is enough to confirm a policy exists and identify the provider.

Also check for correspondence from financial advisers or insurance brokers. Advisers are required to keep records of policies they arranged. If the person used a financial adviser, contact that firm directly — they can tell you what policies they know about, even if they no longer manage them.

Method 2: Check bank statements for premium payments

Go through bank and credit card statements looking for regular outgoing payments to any insurance company. Life insurance premiums are typically monthly or annual direct debits from a current account. The insurer's name will appear in the transaction description.

Look at statements from several years back, not just recent ones. Some older whole-of-life policies have premiums that have been fully paid up — meaning there are no current payments to find, but the policy is still in force. If you find an old payment that stopped several years ago, it may indicate a paid-up policy rather than a cancelled one.

Method 3: Contact their employer or former employers

Contact the HR or pensions department at the deceased person's employer. Ask specifically whether they had a death-in-service benefit as part of their employment package. Also ask about any group life insurance scheme operated by the employer through a pension provider.

If the person was retired, contact their former employer. Death-in-service benefits sometimes extend to deferred pension members, and some pension schemes include a lump sum death benefit paid to a nominated beneficiary. The Pensions Tracing Service at gov.uk/find-pension-contact-details is free and can help trace pension scheme contacts.

Method 4: Use the ABI life insurance tracing service

The Association of British Insurers runs a free tracing service that allows families to search for life insurance policies held by a deceased person. The ABI contacts its member insurers and asks them to check their records. You will need the person's full name, date of birth, and date of death. Results typically take up to six weeks.

This is the most systematic method for finding policies you have no paperwork for. It covers the major UK life insurers. Smaller or older providers may not be ABI members, so a nil result does not completely rule out a policy — but it covers the large majority of policies sold in the UK.

Method 5: Check the unclaimed assets register

The mylostaccount.org.uk service run by the British Bankers' Association, Building Societies Association, and National Savings allows free searches for dormant bank accounts. For insurance specifically, the My Lost Account service covers some dormant policies. Separately, the Unclaimed Assets Register (myunclaimedassets.co.uk) charges a small fee and covers a wider range of financial products including life insurance.

| Method | What it finds | Cost | Timescale |

|---|---|---|---|

| Search paperwork and email | Any policy with documents or correspondence | Free | Hours to days |

| Bank statement search | Active policies with monthly/annual premiums | Free | Hours |

| Employer contact | Death-in-service benefit; group life schemes | Free | Days to weeks |

| ABI tracing service | Policies held with ABI member insurers | Free | Up to 6 weeks |

| Mylostaccount.org.uk | Dormant accounts and some insurance products | Free | Days |

| Unclaimed Assets Register | Wider range including older policies | Small fee | Days to weeks |

The ABI life insurance tracing service: how it works

The ABI's unclaimed assets tracing service is the most widely used formal method for finding out if someone had life insurance in the UK. Here is exactly how to use it.

Submit a request via the ABI's website at abi.org.uk. You will need to provide the deceased person's full name, date of birth, date of death, and last known address. You will also need to confirm that you are an authorised person to make the enquiry — typically the executor of the estate, a beneficiary named in the will, or a close family member.

The ABI sends the details to its member insurers, each of which searches its own records. Insurers respond to the ABI within a set timeframe. The ABI then consolidates the responses and tells you which, if any, members have a matching record. If a match is found, the insurer will contact you directly to begin the claims process.

A nil response from the ABI does not confirm there was no policy. It only confirms that no current ABI member insurer has a record matching those details. The person may have had a policy with a provider that was subsequently acquired, merged, or rebranded — in which case the current entity should still hold the records, but the search may need to be conducted separately.

Death-in-service benefit: the policy nobody thinks to check

Death-in-service is a workplace benefit, not a separate life insurance policy. It is typically part of an employee's total compensation package and pays a lump sum to a nominated beneficiary if the employee dies while in employment.

The payout is usually three to four times the employee's annual salary, though some employers offer more, and some offer less. Senior employees or those at larger companies sometimes have death-in-service benefits of five or six times salary. For someone on a salary of £40,000, this means a potential payout of £120,000 to £160,000 — often completely unknown to the family.

Death-in-service is paid to a nominated beneficiary, not automatically to the estate. This means it does not go through probate and is not subject to inheritance tax in most cases. However, if the employee never nominated a beneficiary — or if the nomination was not updated after a major life event like marriage, divorce, or having children — the trustees of the scheme have discretion over who receives the money.

To claim, contact the employer's HR department with a copy of the death certificate. They will direct you to the pension scheme trustees or the group life insurer. The process is separate from claiming on a personal life insurance policy.

The unclaimed assets register and what it covers

The UK government passed the Dormant Assets Act 2022, which expanded the range of assets that can be transferred to the dormant assets scheme after a period of inactivity. This includes life insurance policies where the insurer has been unable to trace the beneficiary after reasonable efforts.

Assets transferred to the scheme go to Reclaim Fund Ltd, which holds them on behalf of the original owner. The money is not lost — it can be reclaimed at any point. Reclaim Fund Ltd passes unclaimed funds on to good causes, but must pay back the original amount if a legitimate claim is made.

The practical implication for families searching for a policy: a nil result on the insurer search or the ABI tracing service does not mean the money has gone. If the policy existed and the insurer could not trace the beneficiary, the funds may now be held by Reclaim Fund Ltd and can still be claimed. This is a much later step — exhaust the ABI tracing service and direct insurer contact first.

When you find a policy: making a claim

Once you have identified that a policy exists and which insurer holds it, the claim process is relatively straightforward. Most insurers have a bereavement team that handles claims and can talk you through the paperwork.

You will typically need to provide: a completed claim form from the insurer, the original policy document or policy number if available, a certified copy of the death certificate (not a photocopy), and in some cases a copy of the grant of probate or letters of administration if the policy is being paid into the estate rather than to a named beneficiary.

Most straightforward term life insurance claims are settled within two to eight weeks of the insurer receiving a complete set of documents. Claims involving coroner's inquests, investigations into the cause of death, or disputes over who the beneficiary should be take longer. The insurer is legally required to handle claims promptly and can face regulatory penalties for unreasonable delays.

If the claim is rejected or you believe the insurer has handled it unfairly, you can raise a complaint with the Financial Ombudsman Service. The FOS is a free, independent service that adjudicates disputes between consumers and financial services firms.

How to make sure your own life insurance is findable

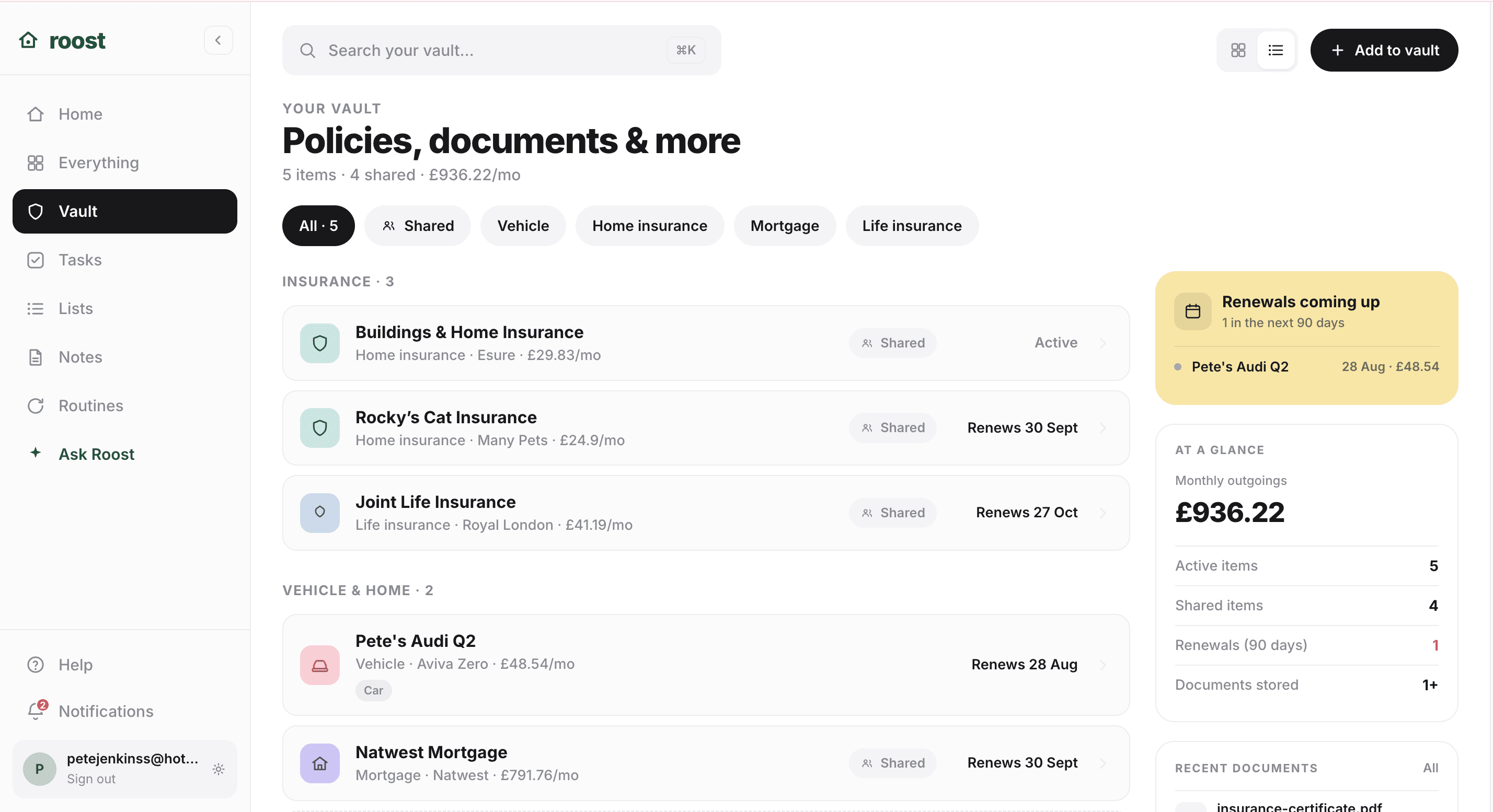

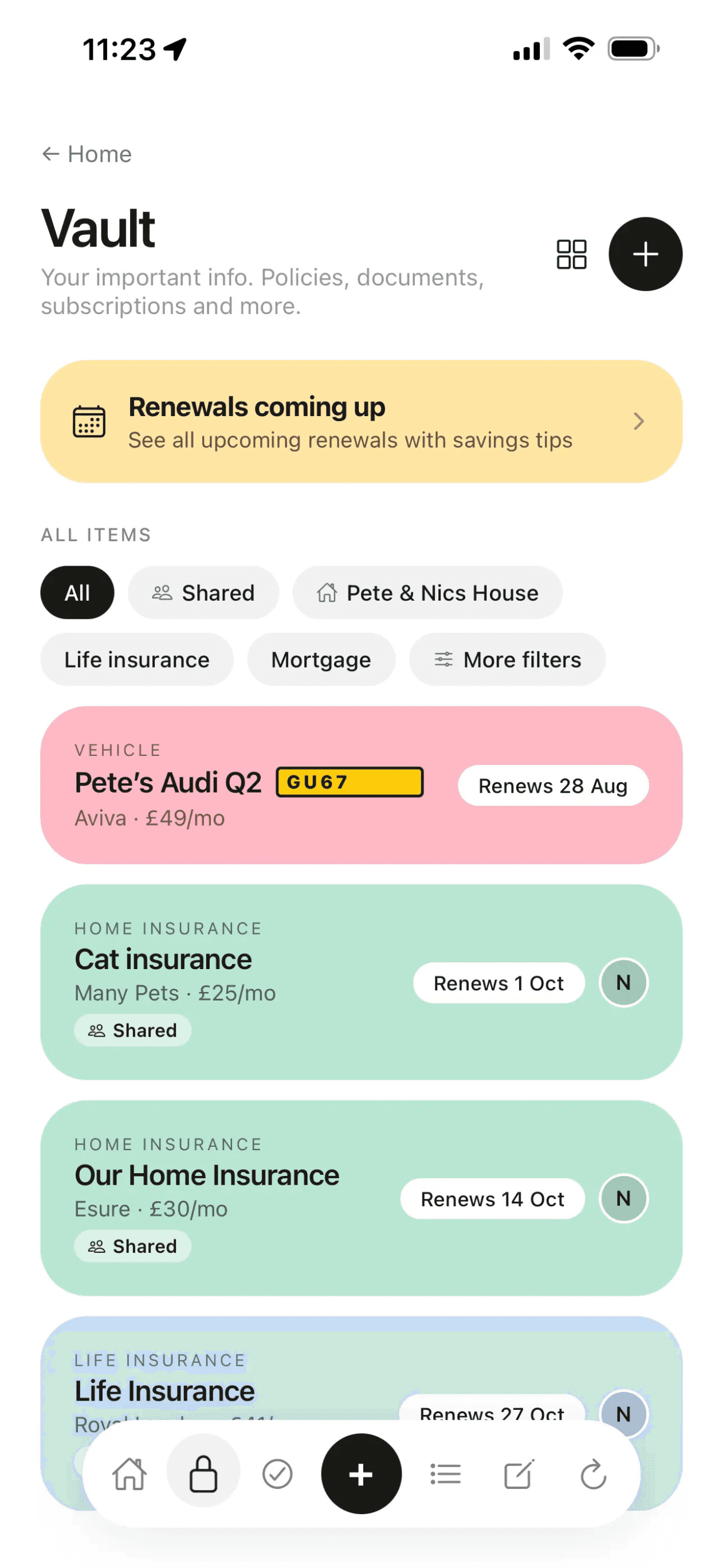

The most useful thing you can do for your own household is to store your life insurance details somewhere your partner or family can find them without knowing what they are looking for. This is not a task that requires legal advice or a formal document — it requires writing down five pieces of information and sharing them.

The five things to record: the insurer's name, the policy number, the approximate cover amount, who is nominated as beneficiary, and where the policy documents are kept (physical or digital). If you have a financial adviser who arranged the policy, add their contact details too.

None of this information is sensitive in the way that a bank account password is sensitive. No one can make a claim on a life insurance policy without a death certificate and evidence that they are the named beneficiary. Recording and sharing the policy details with your household creates no security risk — it only makes it easier for the people who would actually need it.

Review the nominated beneficiary once a year or after any significant life event: marriage, divorce, having children, a bereavement in the immediate family. The insurer will pay the nominated beneficiary regardless of what a will says — the nomination is the instruction the insurer follows.

Roost's vault has a finance section for storing exactly this: insurer name, policy number, cover amount, nominated beneficiary. Free to add, shared with your household, findable in seconds. Start at getroost.io.

Keep it all in one place.

Roost stores your household details, renewal dates, and emergency info — shared with your partner. Free to start.

Quick recap

- To find out if someone has life insurance UK: check their paperwork and email, bank statements, employer, the ABI tracing service, and the unclaimed assets register

- The ABI tracing service at abi.org.uk is free and covers most major UK insurers — results take up to six weeks

- Death-in-service benefit is often missed: contact the employer's HR department and ask specifically about this workplace benefit

- A nil result from the ABI does not confirm there was no policy — the funds may be held by Reclaim Fund Ltd under the Dormant Assets Act

- When you find a policy: contact the insurer's bereavement team with the death certificate; most claims settle within two to eight weeks

- To protect your own family: record your insurer name, policy number, cover amount, and nominated beneficiary somewhere shared and findable

Frequently asked questions

How do you find out if someone has life insurance in the UK?

Start by checking the deceased person's paperwork, bank statements, and email for any policy documents or premium payments. Contact their employer to ask about any death-in-service benefit. Use the Association of British Insurers' unclaimed life insurance tracing service at abi.org.uk, and check the government's mylostaccount.org.uk register. If the person had a financial adviser, contact them directly.

What is the ABI life insurance tracing service?

The ABI (Association of British Insurers) runs a free life insurance tracing service that lets families search for policies held by a deceased person. You submit a request with the person's details and the ABI asks its member insurers to check their records. Results take around six weeks. The service is available at abi.org.uk.

What happens to unclaimed life insurance in the UK?

Unclaimed life insurance stays with the insurer indefinitely. UK insurers are not legally required to pay out unless a claim is made. The ABI estimates that over £2 billion in unclaimed financial assets exist in the UK, including life insurance. After many years, some policies may be transferred to an unclaimed assets register, but the insurer retains the funds until a claim is submitted.

How long does life insurance take to pay out in the UK?

Most UK life insurance claims are settled within two to eight weeks of the insurer receiving the claim form, death certificate, and any supporting documents. Complex cases, particularly those involving coroner's inquests or investigations into the cause of death, can take longer. Term life insurance policies are generally faster to settle than whole-of-life policies.